Sell-Side Opinions: Accenture (ACN) - Jan 03, 2026

Editor's Notes

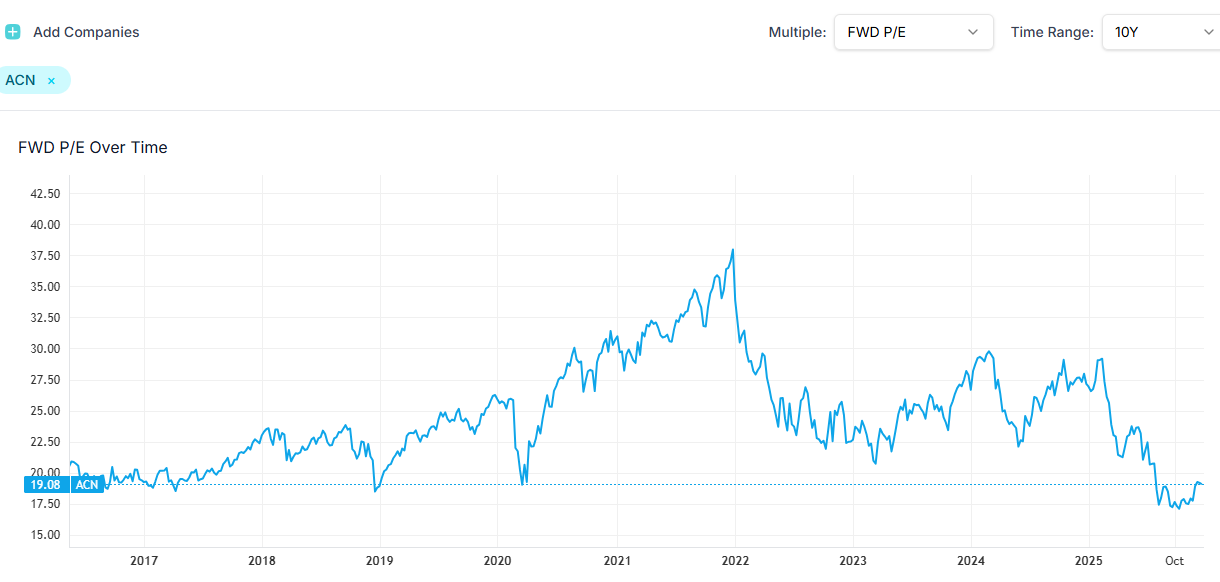

- I mentioned Accenture as a potential target to look into after their Dec 18 earnings in a previous newsletter. Their strong performance vs. AI impact and soft IT cycle phase provided an interesting entry point - multiples close to 10-year low.

- Below is a new experimental synthesis, summarizing sell-side research reports, to distill narratives, projections, consensus and diverging views. Research views largely confirm the limited downside for 2026 performance / stock price ($263 current price vs. $246 bear case by MS), and the ~20% base case upside. I see potential further upside possible if IT spending cycle and AI implementation help drive up topline and margin expansion, as current forecasts build in conservatism and structural skepticism. This is not a multi-bagger, but a cyclical / value bet on slow-growing large-cap leader with high margin of safety and good execution.

- Btw, our call on RH from early Dec is doing very well - up 10% today and 24%+ since our newsletter on Dec 4. Continuing to be bullish on US addressing housing affordability in 2026.

Accenture (ACN) demonstrated strong performance in F1Q26, exceeding revenue and EPS expectations driven by robust bookings in Managed Services and significant AI adoption. Despite persistent macro uncertainties, analysts largely view management's reiterated full-year FY26 guidance as prudent and conservative. Major investment firms maintain 'Overweight' or 'Buy' ratings, citing ACN's strategic positioning in AI, sustained margin expansion, and anticipated gradual market recovery. Key areas of discussion among analysts include the transparency of AI metric reporting and ACN's relative positioning compared to higher-growth IT services peers.

Key Narratives from Recent Accenture (ACN) Research Reports

- Resilient F1Q26 Performance & Prudent Outlook: Accenture delivered a strong F1Q26, with revenue at the top end of guidance and ahead of consensus, coupled with robust bookings and a solid EPS beat. Despite this strength, management maintained its full-year FY26 guidance (2-5% CC revenue growth), a move widely viewed by analysts as prudent and conservative given persistent macro uncertainties and the seasonally challenging F2Q (holiday period, client budget finalization).

- AI as an Embedded Growth Driver: Advanced AI continues to be a significant contributor, driving substantial bookings and revenue growth. Accenture's decision to cease separate reporting for "advanced AI" metrics is framed by some as AI becoming an integral part of all offerings, a sign of its pervasive influence. New ecosystem partnerships with AI model builders (e.g., OpenAI, Anthropic) are highlighted as strategic enablers.

- Improved Operational Efficiency & Margins: Gross margins expanded year-over-year, attributed to improved pricing, contract profitability, and ongoing productivity gains. The recently completed business optimization program is seen as contributing to this margin strength and is characterized as an offensive strategy.

- Shift to Larger, Outcome-Based Deals: Managed Services continues to outpace Consulting, reflecting a client preference for large-scale, transformative, and often fixed-price/outcome-based projects. This trend, coupled with a steady but muted discretionary spending environment, points to a flight to quality and efficiency among clients.

- Stabilizing Macro Environment (Gradual Recovery): While the broader macro environment remains uncertain for discretionary spending, analysts see signs of a gradual bottoming or stabilization in IT services demand. The reduced headwind from the US Federal Services business is also a positive indicator.

Accenture (ACN) Catalysts for Future Growth

- Broadening AI Adoption & Partnerships: Continued integration of AI across Accenture's offerings and strategic partnerships with leading AI model providers are expected to drive client engagement and future bookings.

- Sustained Margin Expansion: Ongoing focus on cost optimization, improved pricing, and efficient delivery models should continue to support margin expansion.

- Rebound in Discretionary Spending: An eventual improvement in the global macro environment and corporate confidence could unlock pent-up discretionary spending, particularly boosting the Consulting segment.

- Strategic M&A: Accenture plans to deploy approximately $3 billion towards M&A in FY26, contributing to growth and expanding capabilities, particularly with an expected acceleration in the latter half of the fiscal year.

- US Federal Business Normalization: The reduced drag from US federal government spending is a positive, with expectations for the headwind to anniversary by FY4Q.

Detailed Projections: Key Metrics for Accenture (ACN)

F1Q26 Actuals (ended Nov 30, 2025):

- Revenue: $18.74B - $18.75B (top end of guidance, +5% FXN y/y).

- Consulting Revenue: +3% FXN y/y

- Managed Services Revenue: +7% FXN y/y

- Gross Margin: 33.1% (up ~20bps y/y).

- Adjusted Operating Margin: 17.0%.

- Adjusted EPS: $3.94.

- Total Bookings: $20.9B - $20.94B (+10% FXN/LC y/y).

- Consulting Bookings: $9.88B (+7.2% y/y)

- Managed Services Bookings: $11.06B (+16.7% y/y)

- AI Bookings: $2.2B (+76% YoY); AI Revenue: $1.1B (+120% YoY). (Note: Last quarter for isolated AI metrics).

FY26 Guidance (Reiterated by ACN):

- Constant Currency Revenue Growth: 2-5%.

- Adjusted Operating Margin Expansion: 10-30 basis points.

- Adjusted EPS: $13.52-$13.90.

- Free Cash Flow: $9.8-$10.5B.

- US Federal Business Headwind: Revised down to ~1% (from 1-1.5% previously).

- GAAP Operating Margin: Tweaked to 15.2-15.4% (from 15.3-15.5%) due to higher restructuring charges ($308M in F1Q).

F2Q26 Guidance:

- 1-5% Constant Currency Revenue Growth (implies sequential deceleration from F1Q).

Analyst Estimates (FY26 / FY27 / FY28):

- J.P. Morgan: FY26 Revenue $73.95B (4.4% FXN growth), FY26 EPS $13.85, FY27 EPS $14.79.

- Goldman Sachs: FY26 EPS $13.90, FY27 EPS $15.00, FY28 EPS $16.40.

- Morgan Stanley: FY26 non-GAAP EPS $13.98, FY27 non-GAAP EPS $15.22.

Scenarios and Valuation Rationale for Accenture (ACN)

- J.P. Morgan (Overweight): Dec-26 Price Target of $302 (up from $290). Valuation based on 20x CY27E adjusted EPS of $15.11. Notes ACN trades at a premium to peers (current NTM P/E 20x vs. peer range of 8-21x). Key risks include deteriorating IT spending, M&A execution, pricing pressure, and talent retention.

- Goldman Sachs (Buy): 12-month Price Target of $330. Valuation based on 22x one-year forward earnings estimates. Sees ACN as best-positioned for recovery in discretionary spending. Downside risks: demand slowdown, AI bookings deceleration, vertical weakness.

- Morgan Stanley (Overweight): Price Target of $320. Valuation based on 21x FY27E EPS ($15.22 consensus), noting it's "modestly above current valuation levels pricing in an 18% discount to the market."

- Bull Case ($390): 24x Bull Case FY27E EPS, assuming accelerating high-single-digit/low-double-digit top-line growth driven by "New" revenue streams, digital transformation, AI partnerships, and diversified verticals.

- Base Case ($320): 21x Base Case FY27E EPS, assuming consistent execution, mid-single-digit CC revenue growth, and 10bps margin expansion.

- Bear Case ($246): 18x Bear Case FY27E EPS, assuming slowing demand or Gen AI cannibalization leading to low-single-digit top-line growth, valuing ACN at a 10-year trough multiple.

Analyst Consensus on Accenture (ACN) Performance and Outlook

- Strong Q1 Performance: All firms agree ACN's F1Q26 results exceeded expectations for revenue and EPS, showing strong underlying execution.

- Prudent Guidance: Analysts uniformly interpret Accenture's reiterated FY26 guidance as a conservative and wise decision, not indicative of weakness but rather management's typical approach in uncertain times and ahead of key client budget cycles.

- Robust Bookings: The double-digit growth in total bookings, especially in Managed Services and AI, is a shared positive observation.

- Margin Expansion: The improvement in gross margins and adjusted operating margins is consistently highlighted as a positive signal for contract profitability.

- Overweight/Buy Ratings: All three major firms (J.P. Morgan, Goldman Sachs, Morgan Stanley) maintain Overweight or Buy ratings on ACN, signaling continued confidence in its long-term prospects.

- Positive Read-Across: Goldman Sachs Japan notes ACN's results imply a positive read-across for Japanese IT services firms with international exposure, suggesting a gradual bottoming of the global IT services market.

Key Debates Regarding Accenture (ACN) Among Analysts

- Interpretation of AI Metrics Reporting Change:

- J.P. Morgan & Goldman Sachs Japan: View Accenture's decision to discontinue separate reporting of "advanced AI" metrics as a natural evolution, implying AI is now so integrated that it's difficult to disaggregate, suggesting success.

- Morgan Stanley: Expresses concern, suggesting it "raises questions around the durability of Gen AI demand and reduces visibility into the pace of project conversion from proof of concept into scaled production." This indicates a desire for continued transparency.

- Investor Conviction on ACN vs. Peers:

- Morgan Stanley ("Stock Performance Review"): Notes that while investors are "looking to get more positive" on ACN, many prefer "higher-beta alternatives such as EPAM and CTSH" due to perceived greater upside and "less structural risk from Gen AI disruption" in ACN's existing segments like SaaS implementation, Song, and Federal. This implies a lingering skepticism about ACN's structural positioning despite strong results.

- J.P. Morgan & Goldman Sachs (main reports): Emphasize ACN's diversified model and strong execution as reasons for confidence, without explicitly noting widespread investor preference for alternatives.

- M&A Efficacy & Returns:

- Morgan Stanley: Expresses caution regarding M&A, citing "limited visibility into the returns of these transactions" and potential for "additional integration costs" despite acknowledging ACN's strong integration track record.

- J.P. Morgan: Views M&A as a positive contributor and optionality, implicitly trusting ACN's ability to execute.

In summary, Accenture's recent performance is strong, with particular strength in managed services and AI. While macro uncertainty and discretionary spending remain headwinds, the company's execution, margin improvement, and strategic positioning in AI and large-scale transformations are viewed positively. The key debate revolves around the transparency and long-term impact of AI, as well as investor conviction on ACN's relative positioning compared to higher-beta IT services peers. Most analysts maintain a positive stance, raising price targets slightly, reflecting the solid quarter and a cautious but optimistic outlook for a gradual market recovery.

Disclaimer: This content is generated using AI, synthesizing public data (filings, reports, news) and social media (Reddit, X). It may contain errors, inaccuracies, or hallucinations. Nothing herein constitutes financial advice. This newsletter is for informational purposes only; please consult a qualified professional and conduct your own due diligence before making any investment decisions.