Pre-Earnings Brief - Jabil (JBL) - Jun 15, 2026

1. Executive Summary

Jabil Inc. (JBL) is scheduled to report its Q3 FY26 earnings on June 17, 2026. This quarterly print arrives at a critical structural inflection point for the company. Over the past year, the market has undergone a significant paradigm shift in how it values Jabil, increasingly re-rating the stock from a traditional, low-margin Electronics Manufacturing Services (EMS) contract provider to a premium, high-value "picks and shovels" enabler of the global artificial intelligence infrastructure boom.

While the mid-to-long-term secular tailwinds surrounding Jabil's proprietary AI hardware pipeline (liquid cooling systems, 1.6T LRO optical modules, and highly complex power systems) remain robust, near-term operational and macroeconomic cross-currents have emerged. Management's recent cautious tone on June 9 regarding non-AI tech sector volatility, combined with a cluster of executive insider stock sales in the $290 to $340 range, has introduced tactical tension ahead of the print.

This brief provides an exhaustive, institutional-grade analysis of the key battlegrounds for the Q3 FY26 earnings release. It breaks down the mathematical "sandbagging" track record of Jabil's management, analyzes crucial value-chain read-throughs from competitors, and outlines a compelling variant view regarding Jabil’s regulatory and compliance advantages over distressed competitors.

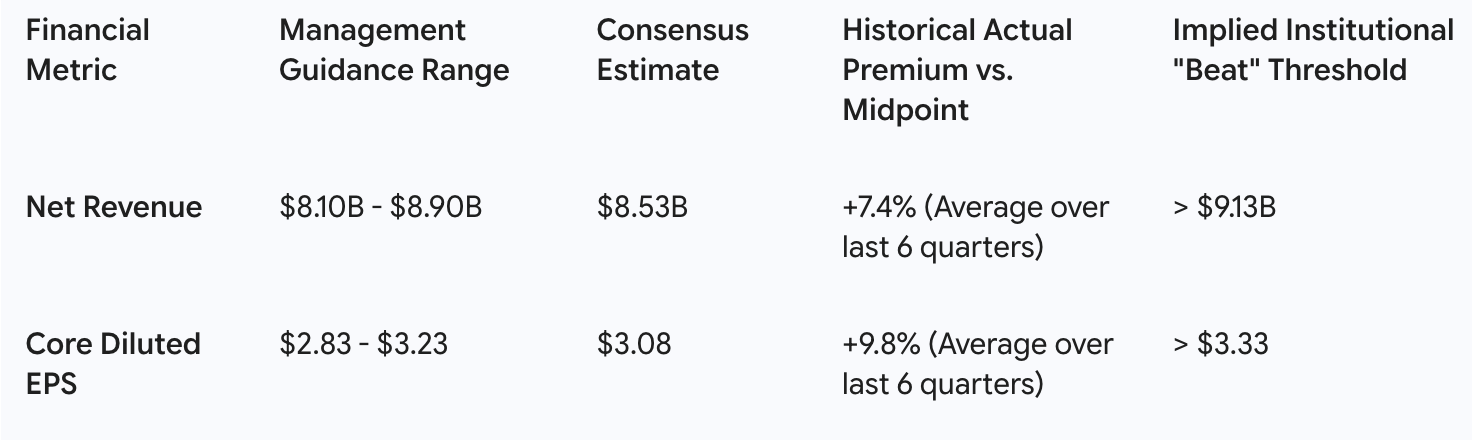

2. Consensus Setup & Historical "Sandbagging" Analysis

A defining characteristic of Jabil's management team is its highly conservative approach to forward guidance—a practice known on Wall Street as "sandbagging." By setting clearing hurdles remarkably low, Jabil has established a predictable multi-year track record of beating guidance and subsequently raising full-year targets.

Investors must evaluate the Q3 FY26 print not merely against the official guidance midpoints, but against the historical "beat premiums" that the market has come to expect.

Q3 FY26 Performance Metrics & Implied Beat Thresholds

Contextualizing the Historical Beat Premium

Over the last six consecutive quarters, Jabil has matched or exceeded the high end of its revenue and Core EPS guidance. The mathematical average of these beats suggests that a simple in-line consensus print of $8.53B in revenue and $3.08 in EPS will likely be viewed as a disappointment by the buy-side. To trigger a sustained post-earnings rally, Jabil must deliver a print exceeding the Implied Institutional "Beat" thresholds outlined above (>= $9.13B revenue and >= $3.33 EPS), which account for the historical management sandbagging premium.

Full-Year FY26 Guidance Context

During previous updates, management upwardly revised its full-year targets, establishing a high baseline of expectations for the remainder of the fiscal year:

- FY26 Consolidated Net Revenue: $34.00 billion

- FY26 Core Operating Margin: 5.7% (with management actively modeling a path toward 6.0% in FY27)

- FY26 Core Diluted EPS: $12.25 per share

3. Core Strategic Pillars & Segment Dynamics

Jabil's ongoing multiple expansion is fundamentally driven by its strategic migration away from legacy, commoditized PC and mobile phone assembly toward high-mix, high-complexity, engineering-led solutions. This transition is organized around two primary pillars:

Pillar A: The Intelligent Infrastructure Growth Engine

The Intelligent Infrastructure segment—comprising cloud architecture, hyperscale data centers, and advanced AI networking platforms—is the crown jewel of Jabil’s portfolio.

- AI Outlook Momentum: Management's upgraded outlook forecasts AI-related revenue to reach $13.10 billion in FY26 (an upward revision from $12.10B, representing a staggering 46% Year-over-Year growth). This growth is driven by secular demand for highly complex AI compute hardware, where Jabil operates as a primary manufacturing and design partner.

- The 1.6T LRO Optical Module Catalyst: Pluggable optical transceivers are critical bottlenecks in high-density AI clusters, where data transfer speeds must keep pace with ultra-fast GPU processing. Jabil’s development of 1.6T LRO (Linear Receive Optical) modules represents a massive, high-margin revenue stream. On June 9, a prominent Key Opinion Leader (KOL) and tech analyst highlighted that Jabil's LRO business was "not yet priced in" by the Street, sparking a 6.96% pre-market stock surge. This business provides Jabil with an proprietary, high-moat technology differentiator that separates it from standard contract manufacturers.

- Capacity Monetization (Pune, India Facility): To meet the explosive backlog for AI-based networking switchgear and 5G infrastructure, Jabil is opening a massive new facility in Pune, India, on the exact day of earnings (June 17, 2026). This launch is a highly visible, physical indicator of execution, signaling that Jabil is rapidly expanding its global manufacturing footprint to support multi-billion-dollar hyperscale partnerships outside of China.

Pillar B: Strategic Margin Expansion vs. Operational Friction

Jabil is aggressively pushing back on the historical belief that EMS companies are permanently capped at a 6% to 7% operating margin ceiling.

- Breaking the Margin Ceiling: Through structural portfolio rationalization, Jabil achieved an outstanding company-wide core operating margin of 6.3% in Q4 FY25. The company's goal is to sustain margins well above 6.0% as high-margin AI infrastructure and complex medical device programs scale.

- Portfolio Rationalization (Clinton, MA Facility Closure): On June 9, Jabil announced the closure of its healthcare manufacturing plant in Clinton, MA, by December 2026, resulting in 103 layoffs. While representing a near-term restructuring drag, this move is a disciplined consolidation designed to optimize manufacturing utilization. By pruning legacy, lower-margin healthcare contracts, Jabil is freeing up capital to focus on specialized, high-growth, high-margin medical vectors, such as continuous glucose monitors and GLP-1 drug delivery systems.

- The "China+1" Capital Expenditure Drag: Geopolitically, Jabil is executing a comprehensive geographic diversification strategy, expanding footprint nodes across Vietnam, India, and Mexico. While this "China+1" strategy is highly attractive to Western hyperscalers seeking to de-risk their supply chains, it introduces short-term capital expenditures, duplicate overhead, and operational friction that could temporarily pressure gross margins during the transition phase.

4. Value-Chain Read-Throughs & Industry Trends

A comprehensive evaluation of Jabil requires analyzing the broader hardware ecosystem. Peer group reports over the past quarter reveal critical structural trends that read directly into Jabil's Q3 print.

Key Peer Read-Throughs:

- AI Infrastructure Demand is Accelerating: Industry bellwethers confirm Jabil's market opportunity. Cisco reported that its AI infrastructure order book has nearly doubled, reaching a $9.00 billion pipeline for FY26, backed by structural resource reallocations. Concurrently, Amphenol reported historic connectivity demand driven by NVIDIA’s next-generation Blackwell systems. These data points validate the underlying strength of Jabil's Intelligent Infrastructure target market.

- Margin Pressures for Low-Complexity Server Integration: In contrast, Super Micro Computer (SMCI) recently engaged in aggressive price-cutting and margin-dilutive pricing strategies to win high-volume server orders, compressing its gross margins and introducing high volatility. This dynamics highlights the danger of low-complexity hardware assembly and underscores the value of Jabil's highly differentiated, high-mix liquid cooling and optical portfolio, which is insulated from commodity server price wars.

- The Struggle of Unoptimized Legacy Businesses: Peer competitor Flex recently spun off its high-growth cloud and power infrastructure business, leaving its remaining legacy segments exposed to low growth and poor free cash flow. This operational divergence highlights the wisdom of Jabil's integrated, diversified approach, which uses reliable cash flows from regulated industries to fund rapid capacity expansions in AI.

5. The Variant View: The Trust, Compliance & Governance Premium

The Street is underestimating Jabil's ability to capture massive, high-margin market share from distressed competitors due to its superior compliance and regulatory infrastructure.

While sell-side analysts focus almost exclusively on aggregate GPU shipment volumes and quarterly server allocations, a major quiet market-share shift is underway. Jabil’s primary competitor in the high-density AI server and rack space, Super Micro Computer (SMCI), is currently facing severe legal, governance, and credibility challenges. These include high-profile auditor resignations, extensive accounting investigations, and the loss of a major $1.00B - $1.40B Oracle contract due to alleged illicit AI GPU exports to restricted regions.

The Jabil Compliance Advantage

In the highly regulated world of hyperscale data centers, compliance and supply chain security are no longer secondary considerations—they are mission-critical requirements. Risk-averse enterprise clients and sovereign cloud providers cannot afford the operational risk of a key manufacturing partner facing export bans or financial delisting.

- Jabil boasts decades of operational maturity, clean regulatory track records, and impeccable international trade compliance infrastructures.

- As hyperscalers seek to de-risk their supply chains away from politically sensitive or operationally unstable vendors, Jabil is positioned as the natural beneficiary of displaced business.

- This "compliance premium" is highly sticky. If Jabil secures even a fraction of SMCI's displaced pipeline, it could drive an accelerated, high-margin organic growth phase in the Intelligent Infrastructure segment that current Street models have completely failed to discount.

6. Landmines & Watch Items for the Q3 Print

Despite the compelling bullish thesis, investors must remain highly alert to several potential negative indicators and risks during the earnings release:

- Reconciling Cautious Near-Term Guidance: On June 9, Jabil’s management issued surprisingly cautious commentary regarding near-term tech sector volatility, driving a ~2% drop in the stock. If management emphasizes non-AI macroeconomic weakness (e.g., Connected Living, digital commerce, or EV/renewables slowdowns) over their AI momentum during the call, the stock could experience a sharp post-earnings sell-off.

- The Insider Selling Disconnect: A cluster of executive stock sales occurred in April at prices between $290 and $340. Although executives sell stock for many reasons, these sales occurred just as Jabil's stock was breaking out. The Street will demand reassurance that these sales do not imply management believes the valuation has temporarily peaked relative to near-term execution capabilities.

- Supply Chain and Component Bottlenecks: The entire AI hardware value chain is constrained by tight supplies of high-bandwidth memory (HBM) and advanced, high-layer printed circuit boards (PCBs). Any commentary suggesting Jabil is experiencing difficulty sourcing these components could indicate that revenue recognition is being pushed out into future quarters.

7. Key Questions for the Earnings Call

An analyst looking to pressure-test Jabil's operational execution and strategic outlook should focus on these five critical inquiries during the Q&A session:

- Optical Module Commercialization & Margins:"Given the recent market enthusiasm surrounding the 1.6T LRO pluggable optical transceivers, can management outline a precise timeline for customer qualification and high-volume manufacturing ramp? Furthermore, how should we think about the margin profile of this optical business relative to the corporate average?"

- Reconciling the Guidance Incongruity:"How should we reconcile the cautious commentary issued on June 9 regarding near-term tech sector volatility with the robust, upwardly revised target of $13.10B in AI-related revenue for FY26? Are you observing any divergence in demand between your hyperscale customers and your broader enterprise client base?"

- Capturing Displaced Market Share:"Without naming specific competitors, are you seeing an acceleration in your customer funnel or receiving active inbound queries from hyperscalers seeking to diversify their manufacturing footprint toward more compliant, stable EMS partners in light of recent industry governance challenges?"

- Healthcare Footprint Transition & Specialized Growth:"Following the planned closure of the Clinton, MA manufacturing plant, what is the expected financial drag from restructuring charges over the next few quarters, and how quickly can Jabil transition its high-margin healthcare programs, specifically for GLP-1 drug delivery systems, to other optimized facilities?"

- Capital Allocation & Valuation Dynamics:"In light of Jabil's robust free cash flow generation and the recent executive share sales in the $290 - $340 range, how does the board view the attractiveness of share repurchases at current valuation levels versus allocating capital to physical capacity expansions, such as the new Pune, India facility?"

Disclaimer: This content is generated using AI, synthesizing public data (filings, reports, news) and social media (Reddit, X). It may contain errors, inaccuracies, or hallucinations. Nothing herein constitutes financial advice. This newsletter is for informational purposes only; please consult a qualified professional and conduct your own due diligence before making any investment decisions.